22 Things You Can Do in 2022 to Maximize Business Value (Part 1)

In this series we’ve already talked about budgeting, succession planning, and building your Green Box, and Growth. Today, we’re going to start a 2 part close to that series - where I’m going to give you 22 things (11 this week, and 11 next week) for you to do in 2022 to maximize your business value!

If you’ve been reading this series, you’ll find a few things we already addressed peppered in. But - there’s much more! Here we go!

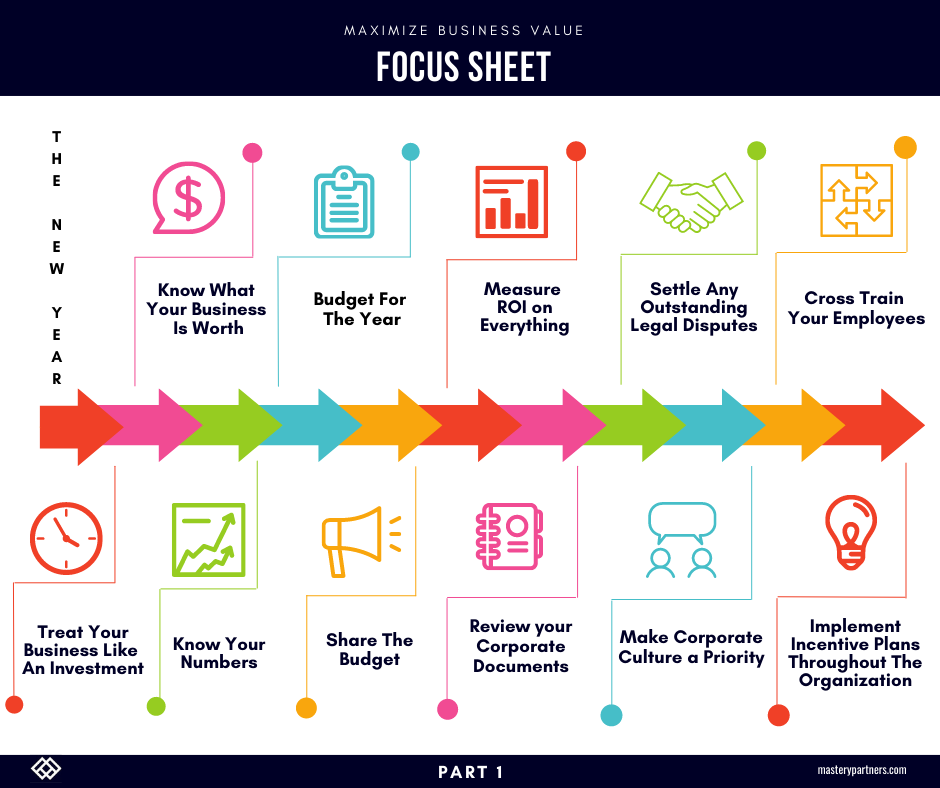

#1 - Treat Your Business Like An Investment

A business is an investment. It’s not a job. It’s not a child. It’s an asset.

Many business owners start their business because of some need. Perhaps it was a need for a new product or service. Perhaps it was a need to secure income after a job loss. Perhaps it was simply to be the boss.

Way back in the beginning - it was exciting. It was new nearly every day. It stretched beyond any reasonable comfort zone. And every owner dreams about the day they’ll sell the business and retire rich.

Unfortunately, somewhere along the way - perhaps once a desired income was reached - it became a job for most business owners. The business became successful, by society’s standards, and the business owner started enjoying all of the trappings of being a successful business owner.

It is at that very same moment the owner stops thinking about the business as an asset and switches to maintenance mode. They need to maintain their standard of living, and so maintenance and risk aversion are the new mantra. Now there’s nothing wrong with having a business that delivers a great lifestyle. In fact it’s a wonderful thing. But, that’s just a stable job, afterall.

Over time, the owner starts thinking about the business as a child. How many business owners have described their business as their “baby?” Well, I’m sorry to say that it’s not. It’s an asset. It’s an investment. The business owner invested time and money to build this business and now it’s likely to be their most valuable asset.

Business owners should treat it like an asset. An asset needs care and attention, just like a home or a boat or a classic car. When those assets need attention, we perk up and take action. A business should be no different.

Business owners should take action every day, every month, every year to increase the value of that asset so that, over time, once a transition occurs, it will keep delivering to support the lifestyle they have become accustomed to and deserve.

#2 - Know What Your Business Is Worth

The number one reason most transitions fail to reach the finish line is most business owners don’t understand the enterprise value of their business. The simple fact is that many business owners have an unrealistic expectation of enterprise value. They haven’t taken the time to understand how businesses are valued in their space or obtained an estimate of the value of the business. That’s a big mistake. We provide an annual valuation update for our clients to ensure they’re tracking in the right direction.

It’s important to have the right expectations when it comes to enterprise value. We provide a free estimate of enterprise value for any business - just click the link at the bottom of our website - www.masterypartners.com.

*BTW - we’re also starting a new Maximize Business Value MasterYclass - Participants get an Opinion of Enterprise Value - so if you sign up, you can cross this one off the list. More information is available at www.MBVMasterYclass.com.*

#3 - Know Your Numbers

Every business owner needs to know their numbers. But you won't know them unless you get your financial statements in a timely fashion! So, let me ask you - How frequently do you get your financial statements?

I'm astounded by the number of times I have talked to business owners who say they don't use interim financial statements. Instead, they get them at the end of the year when the accountant does the taxes. Business owners need to review the financial statements on a routine basis, at least monthly by the 15th. Earlier if possible.

A financial statement is nothing more than a history book. But, it's a history book that can give you clues to the changes that need to happen in order to hit your financial targets. The quicker the owner has the information, the more likely they can change course. There is not a lot of action you can take on history if it's not fresh. The quicker you get a financial statement closer to the beginning of the month, the more likely you can take action on something that doesn't look right.

If you get push back from finance and accounting, who might think it is just too hard to produce in 10 to 15 days, challenge them to set a target for minor improvements and then relentlessly monitor the progress. I’m here to tell you that if I could do it in some of my ridiculously complex businesses, anybody can do it. It is easier than you think if you just get started.

Be proactive about getting your financial statements by the 15th. Business owners who look back months later find it hard to remember the details.

#4 Budget For The Year

Taking the time to plan a budget forces you to think strategically about your business. If you have trouble getting out of the “day to day” of running your business, I encourage you to step back and take a day this month to focus on the future. You’ll thank me in a year!

Setting a budget is like setting a target. Imagine, if you will, running a marathon that has no finish line. That’s what it feels like if you don’t have a budget. Budgets help you set goals for revenue and expenses, and will give you a measuring stick to monitor your progress.

I’m a huge fan of setting an aspirational but realistic budget. If nobody believes the budget is achievable, then it gets challenging to hold managers accountable. Which leads me to #5…

#5 - Share The Budget

Your company’s budget is no good if it just sits on a shelf collecting dust. Once you have it, use it. Share the budget with the key people in the business and hold them accountable for the results. It helps to create and use a scorecard that shows key results compared to the budget. Once you assign the numbers on the scorecard to key individuals, they’ll know exactly how their results are being measured.

Creating the budget should be a team exercise. Otherwise, the team will resent the numbers, and it will give them every opportunity to make excuses for missing the budget. If the group is involved in making the budget, it becomes their budget, not the owner's unrealistic numbers. And if it’s their numbers, it’s easy to hold them accountable.

#6 - Measure ROI on Everything

The long-running joke in my businesses is that if I couldn’t articulate the ROI (return on investment) on toilet paper, we would not purchase it. (Fortunately for my employees and me, I understand the ROI of toilet paper!)

Of course, that is just tongue in cheek, but it does point out an essential tenet of my business philosophy... Measure ROI on EVERYTHING!

Fundamentally, the reason every business owner starts a business is to get a return on investment. Perhaps that investment is capital or time (sweat equity) or a combination of both, but every owner wants a return on their investment at the end of the day. Why shouldn’t that apply to everything else?

I’m a huge risk-taker. I have very few barriers to making investments. (Just ask my wife!) However, I only pull the trigger on investments if I can clearly articulate the return on that investment. This guiding principle is especially true the closer a business is to transition. Any investment made that does not deliver a return before the anticipated transition lowers enterprise value. On the other hand, investments that start paying returns before the anticipated transition will provide a strong argument for increased enterprise value.

It’s worth mentioning that not every investment returns cash. Some investments reduce time to produce results, which lowers cost, which ultimately returns cash and value. So, business owners should base investment decisions on a myriad of factors but ultimately dial them down to the things that increase business value.

#7 - Review your Corporate Documents

Every business has corporate records, and many businesses keep those records in a corporate records book. Whether you keep a book or a file, are your corporate documents up to date? Unless you’re in the tiniest minority of businesses, the answer is NO.

We talk to hundreds of businesses each year, and I always ask that question. When we start our signature Transition Readiness Assessment (TRA) engagement, that is one of the first questions out of my mouth. Of the hundreds of TRAs we’ve completed, the most common answer we hear from clients is ‘no.’ Occasionally, we hear, almost, but they haven’t been updated this year.

These records should include organizational documents, corporate filing receipts, stock certificates, stock ledger, assumed name certificates, board minutes, corporate resolutions (and if you have bank debt - you have surely signed a corporate resolution authorizing that debt for the bank) and more. Even if the business is not required to maintain certain records, like board minutes, it is always good to maintain them anyway.

And make sure everything is in order.

OK - so why is this important to the value of a business?

The fact of the matter is that every business on the planet will eventually transition. When it is time for a business to transition, particularly if the business sells to a 3rd party, the buyer will put the seller through due diligence. Due diligence is the process of reviewing all of the business records to ensure that the seller has appropriately represented the business. However, having been through due diligence over 100 times in my businesses, I can tell you that due diligence is designed for one thing and one thing only - to adjust the purchase price.

One of the first things a buyer will ask for in due diligence is the corporate records. If the corporate records are incomplete or unorganized, the buyer will dig in because this is a sign that perhaps additional things are not being properly maintained. This disorganization will make the buyer wonder what else they are going to find. On the other hand, when records are organized and accurate, this indicates to the seller that the documents are in order and moves the process along much faster. Disorganized records just slow down due diligence, and if there is one thing a seller wants, it’s a speedy due diligence process—the quicker the due diligence, the faster the closing. So - get your corporate records in order!

#8 - Settle Any Outstanding Legal Disputes

Lawsuits accomplish one thing for sure - they make lawyers rich. (OK, that’s a cheap shot, and most lawyers don’t deserve it. But the good ones will agree!)

In my experience, most lawsuits are not worth the effort. I’d have a hard time thinking of a really good reason to file a lawsuit. But it’s taken me a long time to get to that opinion. I've filed lawsuits and fought legal battles on principle before. In retrospect, almost none of them were worth the tens of thousands of dollars in legal bills and countless hours in discovery, depositions, and trial prep that distracted me from running my business.

Let me give you a great example that stands out for me. Many years ago, a customer filed a lawsuit against my business, alleging that our product destroyed his business. After repeated attempts to settle the matter, the client would not budge unless we refunded his entire purchase price. Because we had a firm legal standing in the matter, and unfortunately, it boiled down to a matter of principles for me, we stood our ground and fought the suit. We eventually won the case in court, but the judge admonished me for not settling this matter before it got to his courtroom. The nerve.

So, let’s analyze what we “won.” The original sale of the product to the customer was under $15,000. It cost us over $30,000 in legal fees and hundreds of hours in time. Was it worth it? You do the math.

Look, we live in a highly litigious environment. Lawsuits will come up from time to time. Business owners should think rationally to find a way to settle them amicably - especially the closer the business is to a transition. Any business caught in a legal dispute will find it hard to transition, and the business value could suffer in the meantime.

#9 - Make Corporate Culture a Priority

It’s the little things that mean everything. When a business owner adds all the little things up, they have the equation for a great culture. I think the most important role of any CEO is to be the chief culture officer. Culture is not an event or even a series of events. It is a way of life. A friend of mine recently defined corporate culture as ‘how people act when no one is watching.’ I love that.

Early in my career, I learned from one of my many mentors that if a business owner takes care of their people, they will always take care of the customers.

You don’t have to look very far to find one of the thousands of studies on what motivates employees. And most of those studies show that money comes way down the list of things that motivate people. Recognition, on the other hand, almost always appears at the top of those lists.

A business with a great culture always drives higher values than one with a toxic culture.

#10 - Cross Train Your Employees

Cross-training employees is always a good idea in any company, but it’s essential in small businesses. Many small businesses only have one person trained to do various tasks, and most haven’t documented their processes - a dangerous combination. What happens when the one person who knows a critical procedure is in an automobile accident or has a prolonged illness that keeps them out for weeks or even months? Of course, the business will muddle through and will probably survive, but not without a great deal of unnecessary pain and suffering.

Through the years, I have found that when I cross-train all employees, they love it. From their perspective, it is a benefit to be cross-trained in areas where they might be interested, and it projects that the business is proactive when it comes to stability.

And, by the way, cross-training applies to the owner too. Suppose all of the tribal knowledge resides in the owner’s head and is not documented elsewhere. In that case, the business may never be able to transition and, at the very least, makes it less valuable.

#11 - Implement Incentive Plans Throughout The Organization

It’s almost always a great idea to put incentive plans in place at every level in the organization.

Most companies have incentive plans in place for sales and management, but not throughout the rest of the organization. I get it because it’s hard to develop a good incentive plan - one that drives results at all levels in the organization. However, businesses that find a way to provide incentives to achieve results in every functional area drive greater results and ultimately higher value for the business.

It’s so important that incentives be tied to results and not become some sort of entitlement that’s not tied to specific targets. The best way to do this is to determine the most important objectives for each job in the organization, objectives that drive higher value of the business, and then tie incentives to them. And, there should always be a profitability component. It doesn’t make sense to pay incentives if the business is unprofitable, so the objectives should have some earnings component.

Incentives don’t have to be monetary either. There are all sorts of creative ways to provide incentives to employees. I’ve used parties, lunch trips to bowling alleys, and even a dunking booth (on a rather cold day in Chicago, much to my chagrin), as incentives to achieve team targets. Studies show that most employees are not money motivated. So, find out what motivates the team and use that as the incentive.

Get clear about your objectives and the levers that drive value so you can use them to put incentive plans in place.

So - there are 11 things you can do right now - Next week, I’ll give you 11 more so you’ll have 22 things you can do to Maximize Business Value in 2022!

Call to Action:

Which one of these 11 things will you start TODAY?? It’s never too early to start maximizing your business value - so start right away. If you want me to hold you accountable - just shoot me an email and I’ll follow up with you!

If you need any help, just go to our website and click the button to schedule a call with me. And remember, we’re here to help. If we can help you in any way don’t hesitate to reach out!

Want to learn more? Check out our podcast:

ABOUT THE AUTHOR

Tom Bronson is the founder and President of Mastery Partners, a company that helps business owners maximize business value, design exit strategy, and transition their business on their terms. Mastery utilizes proven techniques and strategies that dramatically improve business value that was developed during Tom’s career 100 business transactions as either a business buyer or seller. As a business owner himself, he has been in your situation a hundred times, and he knows what it takes to craft the right strategy. Bronson is passionate about helping business owners and has the experience to do it. Want to chat more or think Tom can help you? Reach out at tom@masterypartners.com or check out his book, Maximize Business Value, Begin with The Exit in Mind (2020).

Mastery Partners, where our mission is to equip business owners to Maximize Business Value so they can transition their business on their terms. Our mission was born from the lessons we’ve learned from over 100 business transactions, which fuels our desire to share our experiences and wisdom so you can succeed.

Comments